Medicare Costs 2026: Preparing for Potential 8% Increase

Anúncios

Preparing for an anticipated 8% increase in Medicare Costs 2026 Increase, encompassing premiums and deductibles, is essential for beneficiaries to maintain financial stability and access to healthcare.

As we look ahead, the prospect of an 8% increase in Medicare Costs 2026 Increase, including premiums and deductibles, looms large for millions of Americans. This potential adjustment could significantly impact your retirement budget and access to vital healthcare services. Understanding these changes now is not just prudent; it’s essential for proactive financial planning and ensuring your future well-being. This article delves into what these projected increases mean for you and how to navigate them effectively.

Anúncios

Understanding the Projected Medicare Cost Hike for 2026

The anticipation of an 8% increase in Medicare costs for 2026 is a significant concern for current and future beneficiaries. This projection is rooted in various economic factors, healthcare utilization trends, and legislative considerations that influence the program’s financial sustainability.

Anúncios

Such an increase would not be unprecedented, as Medicare costs have historically adjusted to reflect inflation and the evolving landscape of medical care. Understanding the underlying reasons for this projected hike is the first step towards preparing for its impact on your personal finances.

Factors Driving the Increase

Several key factors contribute to the upward pressure on Medicare expenditures. These elements collectively paint a picture of why beneficiaries might see higher costs in the near future.

- Healthcare Inflation: The rising cost of medical services, prescription drugs, and hospital care directly impacts Medicare’s budget.

- Increased Utilization: An aging population means more people are accessing Medicare benefits, leading to higher overall program costs.

- Advancements in Medical Technology: While beneficial, new treatments and technologies often come with a substantial price tag.

- Economic Conditions: Broader economic trends, including wage growth and inflation, influence how Medicare’s funding is calculated and distributed.

These factors create a complex environment where balancing the program’s solvency with beneficiary affordability becomes a continuous challenge. The projected 8% increase reflects an attempt to address these pressures.

In essence, the projected cost hike for 2026 is a multifaceted issue driven by the natural progression of healthcare economics and demographic shifts. Being aware of these drivers empowers beneficiaries to better understand the rationale behind the changes.

Impact on Medicare Part B Premiums and Deductibles

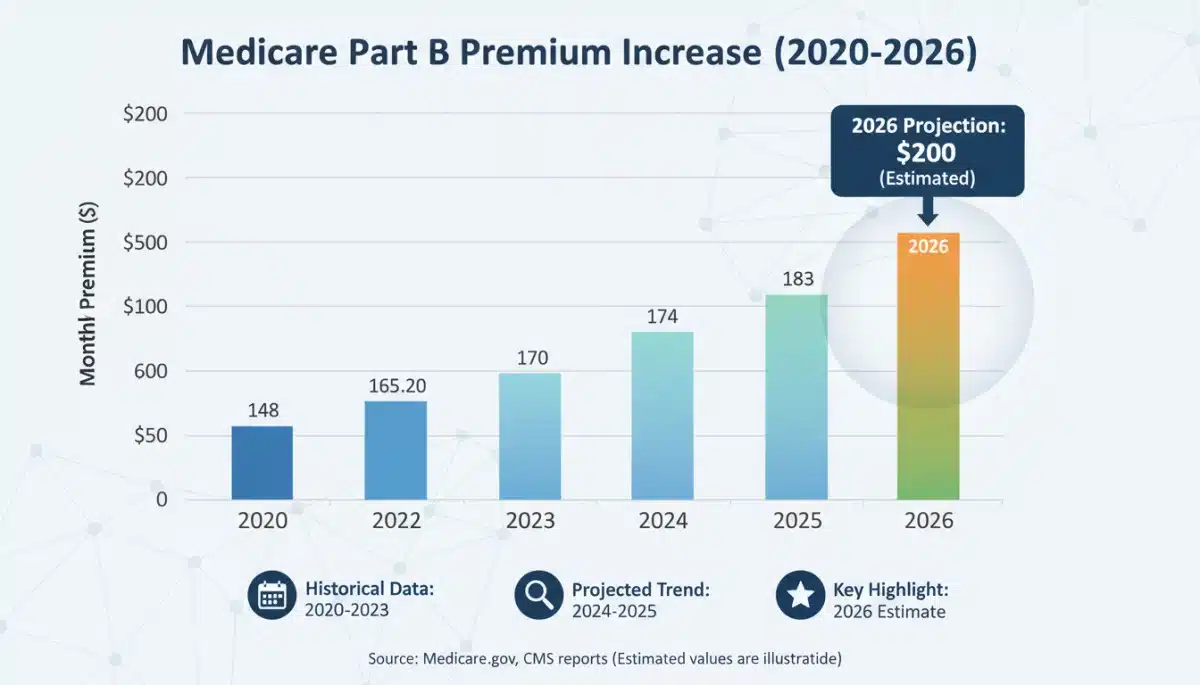

The projected 8% increase will likely manifest most directly in Medicare Part B premiums and deductibles. Part B covers outpatient care, doctor visits, and some preventive services, making its costs a significant component of many beneficiaries’ healthcare budgets.

An increase in these specific areas means a direct financial adjustment for millions. It’s crucial to distinguish between premiums, which are monthly payments, and deductibles, which are the amounts you must pay out-of-pocket before Medicare begins to cover costs.

For example, if the Part B premium currently stands at approximately $174.70 in 2024, an 8% increase could push it well over $188 per month by 2026. Similarly, deductibles would see a proportional rise, meaning you’d pay more before your coverage fully kicks in.

Understanding Part B Premium Adjustments

Medicare Part B premiums are often adjusted annually, based on various economic indicators and the overall health of the Medicare trust funds. The projected 8% increase for 2026 suggests a notable adjustment.

- Income-Related Monthly Adjustment Amounts (IRMAA): Higher-income beneficiaries already pay more for Part B. An 8% increase would magnify these surcharges.

- “Hold Harmless” Provision: This provision often protects many beneficiaries from premium increases that would reduce their Social Security benefits. However, it doesn’t apply to everyone or in all situations.

- Standard Premium vs. IRMAA: Most beneficiaries pay the standard premium, but those with higher incomes face additional surcharges, making the increase more substantial for them.

Preparing for these premium adjustments involves reviewing your current budget and considering how an additional expense might impact your monthly outlay. This proactive approach can help mitigate financial surprises.

The deductible for Part B also plays a critical role in out-of-pocket expenses. A higher deductible means you’ll be responsible for a larger initial portion of your medical bills before Medicare starts paying its share. This could particularly affect those with frequent medical appointments or procedures.

Strategies to Mitigate Rising Medicare Costs

Faced with the prospect of higher Medicare Costs 2026 Increase, beneficiaries have several strategies at their disposal to help manage and potentially reduce their out-of-pocket expenses. Proactive planning is key to navigating these financial adjustments effectively.

These strategies range from reviewing your current coverage options to exploring financial assistance programs. Taking the time to understand and implement these approaches can make a significant difference in your annual healthcare spending.

Exploring Medicare Advantage Plans (Part C)

Medicare Advantage plans, offered by private insurance companies, are an alternative to original Medicare. They often include prescription drug coverage and may offer additional benefits, sometimes with lower out-of-pocket costs.

- All-in-one coverage: Many plans bundle Part A, Part B, and Part D, simplifying your healthcare management.

- Cost-sharing structures: Some plans may have lower premiums or deductibles, but often come with network restrictions.

- Additional benefits: Often include vision, dental, and hearing coverage not found in Original Medicare.

Carefully comparing Medicare Advantage plans available in your area can reveal options that might better suit your health and financial needs, potentially offsetting the projected increases in Original Medicare costs.

Considering Medigap Policies

Medigap (Medicare Supplement Insurance) policies help cover some of the out-of-pocket costs that Original Medicare doesn’t, such as deductibles, copayments, and coinsurance. These policies can be invaluable for predictable budgeting.

While Medigap policies come with their own premiums, they can provide peace of mind by limiting your exposure to unexpected medical bills. It’s essential to enroll during your initial enrollment period to avoid higher premiums or denial of coverage due to pre-existing conditions.

Financial Planning and Budgeting for 2026

Effective financial planning is paramount when anticipating an increase in Medicare Costs 2026 Increase. This involves a thorough review of your current budget, identifying areas where you can adjust, and setting aside funds specifically for healthcare expenses.

Ignoring these potential increases could lead to financial strain, compromising your ability to afford necessary medical care. Therefore, integrating these projections into your long-term financial strategy is not just advisable, but critical.

Reviewing Your Current Budget

Start by meticulously examining your current monthly and annual expenditures. Identify how much you currently allocate to healthcare, including premiums, deductibles, co-pays, and prescription drugs. This baseline will help you understand the scale of adjustment needed.

Consider creating a dedicated “healthcare savings” component within your budget. Even small, consistent contributions can accumulate over time, providing a buffer against unexpected or increased costs. Look for areas where you might trim non-essential spending to reallocate funds.

Long-Term Financial Projections

Beyond immediate adjustments, it’s wise to consider the long-term implications of rising healthcare costs. Work with a financial advisor to integrate these projections into your overall retirement plan. They can help you model different scenarios and develop strategies to ensure your financial security for years to come.

- Retirement Savings: Ensure your retirement savings accounts are robust enough to cover increasing healthcare expenses.

- Investment Strategies: Discuss investment options that could help grow your savings to keep pace with inflation and healthcare cost increases.

- Contingency Funds: Establish an emergency fund specifically for healthcare-related unexpected expenses.

By proactively addressing these aspects of your financial plan, you can build a stronger foundation to absorb future Medicare cost increases without undue stress.

Exploring Government Assistance Programs and Resources

For many beneficiaries, managing rising Medicare Costs 2026 Increase can be challenging, even with careful planning. Fortunately, various government assistance programs and resources are available to help those with limited incomes or unique circumstances. These programs can significantly alleviate the financial burden.

Understanding eligibility requirements and application processes for these programs is a crucial step. Many go underutilized simply because beneficiaries are unaware of their existence or how to access them.

Medicare Savings Programs (MSPs)

Medicare Savings Programs (MSPs) are state-run programs that help low-income individuals pay for Medicare premiums, deductibles, and co-payments. There are different types of MSPs, each with varying income and resource limits.

- Qualified Medicare Beneficiary (QMB) Program: Helps pay for Part A and Part B premiums, deductibles, and coinsurance.

- Specified Low-Income Medicare Beneficiary (SLMB) Program: Helps pay for Part B premiums.

- Qualifying Individual (QI) Program: Also helps pay for Part B premiums, with slightly higher income limits than SLMB.

Enrolling in an MSP can lead to substantial savings, making healthcare more affordable. It’s advisable to check with your state’s Medicaid office or local Area Agency on Aging to determine your eligibility and apply.

Extra Help for Prescription Drug Costs

The Low-Income Subsidy (LIS), also known as “Extra Help,” is a federal program that assists Medicare beneficiaries with the costs of Medicare Part D prescription drug plan premiums, deductibles, and co-payments. This program can be a lifeline for those struggling to afford their medications.

Eligibility for Extra Help is based on income and resources, and even if you don’t qualify for a full subsidy, you might still be eligible for partial assistance. The Social Security Administration manages this program, and applications can be submitted online or by phone.

Advocacy and Future Outlook for Medicare

The discussion around Medicare Costs 2026 Increase is not just about personal financial adjustments; it also involves broader advocacy efforts and the future outlook for the program. Understanding these larger forces can provide context and highlight avenues for collective action.

Policymakers, advocacy groups, and beneficiaries all play a role in shaping Medicare’s future. The potential 8% increase underscores the ongoing need for sustainable solutions that ensure both program solvency and beneficiary access to care.

Advocacy for Beneficiary Protections

Various organizations are dedicated to advocating for Medicare beneficiaries, working to protect them from excessive cost increases and ensuring access to comprehensive care. These groups often engage with lawmakers to propose and support policies that address affordability and access.

Staying informed about these advocacy efforts and lending your voice can contribute to a stronger collective impact. Contacting your elected officials to express your concerns about rising Medicare costs is one way to participate in this important dialogue.

Long-Term Sustainability and Reforms

The long-term sustainability of Medicare is a subject of continuous debate and policy discussion. As the population ages, the financial pressures on the program are expected to grow, necessitating ongoing reforms.

- Legislative Proposals: Various proposals aim to reform Medicare’s financing, benefits, and administration.

- Healthcare System Efficiency: Efforts to make the broader healthcare system more efficient can indirectly benefit Medicare by reducing overall costs.

- Preventive Care Emphasis: Promoting preventive care can reduce the incidence of costly chronic conditions, potentially lowering long-term expenditures.

The future of Medicare will likely involve a combination of these approaches, aiming to balance the needs of beneficiaries with the fiscal realities of the program. Staying engaged in these conversations is important for all stakeholders.

| Key Point | Brief Description |

|---|---|

| Projected 8% Increase | Medicare premiums and deductibles are anticipated to rise by 8% in 2026, impacting beneficiary costs significantly. |

| Impact on Part B | Medicare Part B premiums and deductibles will likely see the most direct and substantial increases for beneficiaries. |

| Mitigation Strategies | Options like Medicare Advantage, Medigap, and financial planning can help manage the rising costs. |

| Assistance Programs | Government programs like MSPs and Extra Help offer financial aid for eligible low-income Medicare beneficiaries. |

Frequently Asked Questions About 2026 Medicare Costs

The projected 8% increase in Medicare costs for 2026 is driven by several factors, including healthcare inflation, an aging population leading to increased utilization, advancements in medical technology, and broader economic conditions. These elements collectively put upward pressure on the program’s expenditures.

The projected increase will most directly impact Medicare Part B premiums and deductibles. Part B covers outpatient care, doctor visits, and some preventive services. Beneficiaries may also see adjustments in Part A deductibles and coinsurance, as well as Part D prescription drug costs.

Beneficiaries can prepare by reviewing their current budget, exploring Medicare Advantage (Part C) plans or Medigap policies, and investigating government assistance programs like Medicare Savings Programs (MSPs) and Extra Help for prescription drugs. Proactive financial planning is crucial.

Yes, several government assistance programs are available. Medicare Savings Programs (MSPs) can help pay for Part A and B premiums and deductibles. The Low-Income Subsidy (LIS), or “Extra Help,” assists with Part D prescription drug costs. Eligibility varies by income and resources.

Stay informed by regularly visiting the official Medicare.gov website, consulting with a trusted financial advisor specializing in retirement planning, and subscribing to updates from reputable healthcare news sources. Engaging with advocacy groups can also provide valuable insights and support.

Conclusion

The anticipated 8% increase in Medicare Costs 2026 Increase, encompassing premiums and deductibles, presents a significant financial challenge for millions of Americans. However, by understanding the underlying causes, exploring available mitigation strategies, engaging in diligent financial planning, and leveraging government assistance programs, beneficiaries can effectively navigate these changes. Proactive preparation is not just about managing expenses; it’s about safeguarding access to essential healthcare and ensuring peace of mind in retirement. Staying informed and advocating for sustainable Medicare solutions will be crucial in the years to come.

Access")